September, 2023

Key Contributors

Megaport (MP1, overweight) – our overweight position in the software technology company outperformed following a positive FY23 results and FY24 guidance. FY23 EBITDA increased materially to $20m compared to the prior period loss of $10m with revenue growth remaining strong at +40% yoy. FY24 EBITDA guidance has been upgraded multiples times over recent months with the cumulative uplift in EBITDA expectations over +50%. The solid earnings result was due to stronger than expected pricing and cost reductions. We continue to hold the position as we believe customer volume trends will improve in the medium to long term as execution improves. Furthermore, we would highlight that yield growth, low customer churn, margin expansion (including cost reduction programs) and lowe capex will support a transition to free cashflow positive in CY24 with significant cashflow potential longer term.

Carsales.com (CAR, overweight) -- the online auto classifieds company outperformed during the period following its full-year result. The result proved up CAR’s investment case of the recent acquisitions of Trader Interactive in the US business and Webmotors in Brazil, with both businesses demonstrating double digit yield growth as dynamic pricing models were introduced. Combined with a strengthened market position in Australian private car sales, there is now much greater visibility around continued price and yield increases across the business.

Key Detractors

Iluka Resources (ILU, overweight) – our overweight position in the mineral sands company was a detractor during the quarter. Iluka reported a 10% decline in mineral sands revenue and a 22% decline in underlying EBITDA in its FY23 results, with the market concerned over the short-term outlook for mineral sands demand notwithstanding ILU's commentary of flat pricing in the second half. We continue to like mineral sands markets long-term and favour ILU 's leverage as the world's largest Zircon producer and fifth largest producer of titanium feedstocks. Iluka is moving into Rare Earths production through the Eneabba refinery and should be a critical component producer for the EV industry.

Healius (HLS, overweight) – the pathology and medical imaging company underperformed post the competition regulator (ACCC) raising concerns over its merger with Australian Clinical Labs (ACL). While recent HLS operational performance has been significantly impaired by a combination of below normal pathology volumes (slow rebound in business-as-usual activity following COVID) and elevated operational costs (elevated COVID-testing related costs), we see an opportunity under the new CEO to improve business focus, enhance operational margins and rebuild balance sheet resilience.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Sept-2023.pdfAugust, 2023

Key Contributors

Carsales.com (CAR, overweight) – the online auto classifieds company outperformed during the month following its full-year results. The results proved up CAR’s investment case of the recent acquisitions of Trader Interactive in the US business and Webmotors in Brazil with both businesses demonstrating double digit yield growth as dynamic pricing models were introduced. Combined with a strengthened market position in Australian private car sales, there is now much greater visibility around continued price and yield increases across the business.

WiseTech (WTC, underweight) – the logistics industry software solutions provider underperformed during the period following its full-year result, where earnings guidance for the next financial year fell well short of consensus estimates. The miss was driven by higher-than-anticipated investment expenses and margin dilution from recent acquisitions.

Megaport (MP1, overweight) – our overweight position in the software technology company outperformed following a positive FY23 result and upgraded FY24 guidance. FY23 EBITDA increased materially to $20m compared to the prior period loss of $10m with revenue growth remaining strong at +40% yoy. FY24 EBITDA guidance has been upgraded multiples times over recent months with the cumulative uplift in EBITDA expectations over +50%. The solid earnings result was due to stronger than expected pricing, lower churn and cost reductions. We continue to hold the position as we believe customer volume trends will improve in the medium to long term as execution improves. Furthermore, we would highlight that yield growth, low customer churn, margin expansion (including cost reduction programs) and lower capex will support a transition to free cashflow positive in CY24 with significant cashflow potential longer term.

Key Detractors

Judo (JDO, overweight) – the small to medium business lender underperformed during the period with concerns over NIM (net interest margin) headwinds. Since IPO, JDO has consistently hit its targets and appears on track to achieve its medium-term goals, however lack of detailed FY24 guidance impacted investor confidence. We see JDO as differentiated in the small cap financials space given it is an ADI (authorised deposit-taking institution), allowing it to take deposits and have a relatively lower cost of funding to many other non-ADI peers in the small caps index. Lower funding costs, combined with higher yielding SME loans, should allow JDO to generate a strong NIM of ~3%+ in the medium term. The valuation is attractive with JDO trading at a material discount to book value.

Alumina (AWC, overweight) – our overweight position in the alumina producer was a detractor during the month following its half-year results. We are concerned that environmental approvals to mine, close to the Serpentine dam may not be received in a timely manner, and the company has less than 12 months of remaining low-grade ore to mine at Huntly. We see a material risk that the Kwinana and Wagerup refineries may be forced to curtail production or even close at a time where the company's debt levels are approaching unsustainable levels. This has led us to exit the position.

Iluka (ILU, overweight) – our overweight position in the mineral sands company was a detractor during the month. Iluka reported a 10% decline in mineral sands revenue and a 22% decline in underlying EBITDA in its FY23 results. Additionally, the market was concerned over the short-term outlook for mineral sands demand, notwithstanding ILU's commentary of flat pricing in the second half. We continue to like mineral sands markets long-term and favour ILU 's leverage as the world's largest Zircon producer and fifth largest producer of titanium feedstocks. Iluka is moving into Rare Earths production through the Eneabba refinery and would be a critical component producer for the EV industry.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund_Aug-2023.pdfJuly, 2023

Key Contributors

Megaport (MP1, overweight) – the software technology company outperformed in July following a positive earning guidance upgrade reflecting stronger-than-expected pricing and cost reductions. Confidence in MP1's free cash flow increased which led to the tech company cancelling its (unused) debt facility. We continue to hold the position and expect volume trends will improve in the medium to long term as sales execution improves. Furthermore, we believe that yield growth, low customer churn, margin expansion (including cost reduction programs) and lower capex will support a transition to positive free cashflow in CY24 and with significant cashflow growth potential longer term.

Flight Centre (FLT, overweight) – the travel agent outperformed during the month following an upgrade to guidance on the back of better-than-expected corporate demand and higher margins. We continue to hold an overweight position. FLT’s Leisure division (40% of preCOVID EBIT) is set to benefit from pent-up travel demand, with improved margins after a material reduction in the cost base. The Corporate division (60% of pre-COVID EBIT) is rapidly expanding market share which will more than offset a smaller addressable market caused by increased use of virtual meetings. Furthermore, as group earnings improve, we believe there is additional value to be released from restructuring the balance sheet.

Key Detractors

Iluka (ILU, overweight) – our overweight position in the mineral sands company was a detractor during the month. Despite the company's solid June quarterly production report, ILU expects demand to be softer during 2H23. Competitor Tronox also highlighted this trend which led to market concerns. While we see short-term demand risks, traditional supply sources – particularly in South Africa – appear to be in decline, supporting ILU's expectations for flat pricing in the second half. We continue to favour the mineral sands markets for long-term investment, and specifically ILU as the world's largest Zircon producer and fifth largest producer of titanium feedstocks. Iluka is moving into Rare Earths production through its Eneabba refinery, adding potential for the company to become a critical component producer for the EV industry.

Healius (HLS, overweight) – the pathology and medical imaging company underperformed following the ACCC detailing its concerns over the company’s proposed merger with Australian Clinical Labs (ACL). While recent HLS operational performance has been significantly impaired by a combination of below normal pathology volumes (a slow rebound in business-as-usual activity following COVID) and elevated operational costs (elevated COVID-testing related costs), we see an opportunity under new CEO Maxine Jaquet to improve business focus, enhance operating margins and rebuild balance sheet resilience.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jul-2023.pdfJune, 2023

Key Contributors

NEXTDC (NXT, overweight) – following the announcement of the data centre operator’s largest ever individual contract in April and subsequent regional expansion into Malaysia and New Zealand, NXT continued to outperform as the market’s conviction in Artificial Intelligence (AI) applications as a driver of demand growth grew. Most notably, global leading specialist chip maker Nvidia’s commentary around AI driven demand growth supported previous comments made by NXT management.

Pinnacle Investment Management (PNI, overweight) – the fund manager outperformed during the period, in part supported by stronger than expected inflows of +$1.9bn during the first three months of 2023. Going forward, we believe revenue growth will accelerate with material longer term growth potential as market conditions normalises from depressed levels, inflows re-accelerate across its diverse range of investment products and via international distribution, performance fees increase from near zero at the 1H23 result and new products mature. Furthermore, margin expansion will be supported by the fixed cost nature of funds management businesses and new manager formation both organically and via acquisitions, which we expect will create additional shareholder value.

Key Detractors

Allkem (AKE, underweight) – our underweight position in the lithium producer was a portfolio detractor during the quarter. Lithium carbonate prices rallied from recent lows across the period to end the quarter up 24% at US$41k/t. In addition, AKE announced plans to merge with peer Livent Corporation (LTHM.US), with the merger ratio implying a 7% premium for AKE shareholders. Our preference amongst lithium exposures remains IGO. While we recognize Allkem offers lithium supply diversity across both brine (Olaroz) and hard-rock (Mt Cattlin) operations, we are concerned with its material asset-specific and geopolitical risks.

WiseTech (WTC, underweight) – our underweight position in the logistics industry software solutions provider was a source of underperformance during the period, with WTC benefiting from a rotation into those software names that might benefit from AI developments. We believe WTC is continuing to build an exceptional product in CargoWise which should continue to attract and retain large and key freight forwarders. Despite WTC's high-quality earnings growth, we struggle to justify paying 80-times earnings given the more attractive opportunities available in the sector (e.g. XRO).

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jun-2023.pdfMay, 2023

Key Contributors

NEXTDC (NXT, overweight) – following the announcement of its largest ever individual contract the previous month, the data centre provider continued to outperform as the market’s conviction in Artificial Intelligence (AI) applications as a driver of demand growth grew. Most notably, global leading specialist chip maker Nvidia’s commentary around AI driven demand growth supported previous comments made by NXT management.

Key Detractors

oOh! Media (OML, overweight) – the outdoor media company underperformed in May given short term cyclical headwinds to revenue and higher than expected costs on contract renewals. We continue to hold an overweight position in OML given cyclical media market upside in the longer term, with the outdoor media category set to expand its share of traditional advertising (digital product / improved audience measurement). Lastly, OML is improving its market share of the outdoor category, we expect cost growth will be limited – the company has high fixed cost leverage – and the balance sheet is strong which provides support to the current share buyback.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-May-2023.pdfApril, 2023

Key Contributors

Reliance Worldwide (RWC, overweight) – the manufacturer and distributor of plumbing and heating parts outperformed following the release of its March-quarter trading update. The trading update was broadly positive, demonstrating the resilience of its repair-focussed end markets (total sales growth of +14.2% for the nine months ending March-23) and a robust margin outlook supported by cost-out plans and easing raw material cost pressure. We view RWC as a compelling opportunity, with the market pricing for a significant decline in earnings (P/E of only 14.9 times vs 17.0 times mid cycle) whereas we remain constructive on the demand environment given the defensive nature of RWC's revenue base, the majority of which relates to repair and remodelling sales.

Key Detractors

Telix Pharmaceuticals (TLX, underweight) – radiopharmaceutical company TLX outperformed the market in April after announcing a strong Q123 revenue result. Sales of TLX’s key Illuccix product were substantially stronger than market expectations. This strength was partially driven by higher than anticipated numbers of PSMA-PET scans per patient. Further, a strong result from key competitor Lantheus suggests the overall market volumes are expanding well. We are underweight TLX given our cautious view on the long-term pricing sustainability of radiopharmaceuticals.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Apr-2023.pdfMarch, 2023

Key Contributors

Reliance Worldwide (RWC, overweight) – the manufacturer and distributor of plumbing and heating parts outperformed early in the quarter as the 30-year US mortgage rates compressed ~30bps and the market's belief that the Fed was getting closer to the top of this rate hiking cycle strengthened. RWC also outperformed after its March Investor Day at which it announced two new products which should drive EBIT upgrades in later years (FY25+). We view RWC as a compelling opportunity, with the market pricing for a significant decline in earnings (P/E of only 14.5 times vs 17.0 times mid cycle) whereas we remain constructive on the demand environment given the defensive nature of RWC's revenue base, the majority of which relates to repair and remodelling sales.

Key Detractors

Liontown Resources (LTR, underweight) – the lithium developer outperformed during the period, despite falling lithium prices, following a takeover offer from US-listed lithium producer Albermarle. The $2.50/share offer represented a 63% premium to last close, with the company trading above terms on expectations of a further bump in the bid following its rejection of the initial proposal. We continue to see further downside to lithium prices and prefer existing operator Pilbara Minerals (PLS) given its lower risk profile, strong balance sheet, and low capital intensity growth profile.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Mar-2023.pdfFebruary, 2023

Key Contributors

AUB (AUB, overweight) – AUB outperformed in the month due to a strong 1H22 update which included a guidance upgrade. The result confirmed substantial premium growth trends in the industry, which assisted organic growth. AUB’s recent significant acquisition, Tysers, delivered a solid 1H22 performance which beat previous guidance and confirmed the integration of Tysers into AUB continues to travel well. The core Australian broking business saw good operating leverage, with EBIT margins increasing to 35.2% from 31.1%, and medium-term margin targets increased for various AUB divisions. We continue to hold AUB as the market gains further confidence in the outlook for the Tysers acquisition and continued operating leverage is realised in AUB’s operating divisions.

Flight Centre Travel (FLT, overweight) – the travel company outperformed during the period after announcing a stronger than expected 1H23 result above prior guidance, including positive outlook commentary which touched on the recently acquired premium leisure travel business, Scott Dunn. The Leisure division (40% of pre-COVID EBIT) is set to benefit from pent-up travel demand, with improved margins after a material reduction in the cost base. The Corporate division (60% of pre-COVID EBIT) is rapidly expanding market share, which we expect will more than offset a smaller addressable market caused by the increased use of virtual meetings. Furthermore, as group earnings improve, we believe there is additional value to be realised from restructuring the balance sheet.

Key Detractors

Evolution Mining (EVN, overweight) – the gold producer was a negative contributor during the period. EVN recovered value in late 2022 following disappointing production levels, guidance downgrades and balance sheet concerns during the middle of the year. However, the stock followed the gold price lower in February, with gold declining 5% to US$1,817/oz at month end. We continue to see support for gold prices across the medium term, and see EVN as well placed to benefit from an improving balance sheet, resource upside at Ernest Henry, and further turnaround Potentia at Red Lake.

Pinnacle Investment Management (PNI, overweight) – the investment manager underperformed during the period after reporting a 1H23 result below expectations, largely due to lower-than-expected revenues across both performance and management fees. Going forward, we believe revenue growth will increase, with material longer term growth potential as market conditions normalise from depressed levels, inflows increase across its diverse range of products, performance fees increase from recent near-zero levels, international distribution accelerates, and new products mature. Furthermore, margin expansion will be supported by the fixed cost nature of the funds management industry and new manager formation (organic and via acquisition), which has created material shareholder value over time.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Feb-2023.pdfJanuary, 2023

Key Contributors

Reliance Worldwide (RWC, overweight) – the plumbing supplies company outperformed over the month of January following news of the widespread freeze event in the US in late December. These freeze events occur approximately every three years and this one should provide a solid boost to sales as repairs are undertaken to rectify frozen pipes. US 30-year mortgage rates also compressed ~50bps over the month, a positive move for home renovators that look to draw on their mortgages, with the share price also responding positively to this movement. Looking at the stock more broadly, the market is showing concern for a falling demand environment and RWC FY23 estimates were lowered after the company's August result and 1Q23 update. We believe RWC is a compelling opportunity with the market pricing for a significant decline in earnings (P/E of only 14 times vs 17 times mid cycle), while we remain constructive on the demand environment given the defensive nature of the majority of RWC’s repair and remodelling sales.

Key Detractors

Incitec Pivot (IPL, overweight) – the explosives, fertilisers and industrial chemicals company underperformed over the month as ammonia prices reduced 23% to $790/t. Ammonia prices in Europe have been falling with demand in Asia very soft, the removal of an 5.5% EU import duty & EU gas prices in late December at their lowest level for seven months. We note these movements are temporary rather than structural and note that spot prices are in line with consensus forecasts for FY23. We remain overweight the company, with positive catalysts on the horizon for the stock.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jan-2023.pdfDecember, 2022

Key Contributors

Evolution Mining (EVN, overweight) – our position in the gold miner was a positive contributor during the month, with the gold price rising to US$1,828/oz at period end. Following a period of significant underperformance relative to its listed peers, reflecting disappointing production levels and guidance downgrades, we see attractive valuation support for EVN. While gearing levels – around 30% (D/D+E) – are higher than peers, the risk of an unexpected capital raise to support the balance sheet is considerably overplayed in our view. AUD denominated gold prices remain robust, and we continue to see price support for gold in the near to medium term.

Key Detractors

Reliance Worldwide (RWC, overweight) – the plumbing supplies company underperformed during the period following James Hardie's (ASX listed peer) weaker than expected market update. The market is showing concern for a falling demand environment and RWC FY23 estimates were lowered after the August result. We believe RWC's reaction to JHX's update is un-warranted. We believe RWC is a compelling opportunity with the market pricing for a significant decline in earnings (P/E of only 12 times vs 17 times mid cycle), while we remain constructive on the demand environment given the defensive nature of the majority of RWC's repair and remodelling sales. In addition, the widespread and strong US freeze over the holiday period in late December should provide a strong boost to sales as repairs are undertaken to rectify frozen pipes.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Dec-2022.pdfNovember, 2022

Key Contributors

Evolution Mining (EVN, overweight) – the gold miner was a positive contributor during the month, with the gold price rising 8% to US$1,768/oz at month end. Following a period of significant underperformance relative to listed gold peers, due to disappointing production levels and guidance downgrades, we now see attractive value support for EVN. While gearing levels – around 30% (D/D+E) – remain higher than peers, the risk of an unexpected capital raising to support the balance sheet is considerably over-played in our view. AUD denominated gold prices remain robust, and we continue to see price support for gold in the near to medium term.

Sandfire (SFR, overweight) – the copper producer was a positive contributor to the portfolio during the period. Copper prices increased 9% over the month to close at US$3.73/lb. We like copper as a commodity given its leverage to electrification as a key material in batteries and electric motors. In addition, the company undertook an equity raising during the period which was well received by investors. We participated in the company's $200m Entitlement Offer during the period and view the raising as an important de-risking event for the balance sheet. The company is now better funded to complete the Motheo project in Namibia, and progress drilling activities to increase the mine life at the MATSA asset in Southern Spain. Further de-risking of these projects, coupled with the positive outlook for copper markets, will continue to generate share price outperformance in our view.

Key Detractors

Select Harvests (SHV, overweight) – the almond producer underperformed during the period after a weaker than expected result and outlook. The outlook for the almond price and cost inflation both deteriorated compared to prior expectations. We continue to hold the SHV position given almond prices are currently depressed below sustainable levels, costs are currently abnormally high and the downside is protected by a large tangible asset base including land and water assets.

October, 2022

Key Contributors

Link Group (LNK, overweight) – the company’s share price recovered somewhat during the month following sharp underperformance in the prior month following termination of the agreed deal with Dye & Durham to buy the company. We still see considerable value in LNK and a pathway to crystalizing this value and regard the announced demerger of its stake in PEXA as an appropriate first step. LNK received a substantial bid from Dye & Durham for its Corporate Markets and Banking & Credit Markets businesses during the month which further highlights the value in the constituent parts of LNK.

Nanosonics (NAN, overweight) – the disinfection device company outperformed during the period despite no recent updates. The business continues to perform well with double digit growth in the installed base, the successful transition of the US distribution capability from GE and recovery in the consumables volumes as COVID disruption moderates. Despite this, the stock has been caught up in the growth sell-off and offers compelling value at these levels.

Key Detractors

Megaport (MP1, overweight) – the network as a service solutions company underperformed after releasing its September quarterly result, which was weaker than expected across customer volume metrics and confirmed higher than expected capex. We would note the June quarterly result beat expectations and that the September quarter is a seasonally less important one. Longer term we see strong growth from the core business connecting data centres to the cloud, with a strong global pipeline as businesses invest in IT projects. With its expansion into broader telecommunication services – which leverages the same infrastructure – the total addressable market more than doubles. The company is currently at an inflection point for earnings and cashflow; we believe it will turn positive in the next year with significant long-term earnings and cashflow potential.

OZ Minerals (OZL, overweight) – the copper miner was a negative contributor in October despite no incremental news, with BHP’s takeover offer for the company weighing on share price performance. With the OZL board rejecting the initial offer, we recognize the potential for BHP to return with a higher bid and regard the potential for a counterbidder to emerge as limited, given BHP’s significant available regional synergies. We retain our fundamental positive view on OZL due to its two high quality, long life, 100% owned copper mines in South Australia – Prominent Hill and Carrapateena. We expect the company’s copper production to double to >200ktpa by 2030, as Carrapateena moves to a block caving operation, and the company develops the greenfield West Musgrave copper/nickel deposit in Western Australia.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Oct-2022.pdfSeptember, 2022

The Emerging Leaders Benchmark returned 2.37% for the quarter, taking its 12-month return to -15.28%. In comparison, the broader ASX300 gained 0.45% for the quarter and, globally, the MSCI World Index fell 15.70%.

The Energy and Materials sectors recorded positive returns. Within Energy (+12.4%), coal producers continued to rise in value amid the global energy crisis, with thermal coal reaching an all-time high of $457/t during the quarter. New Hope Corporation (NHC) lifted +81.8% and Paladin Energy (PDN) gained 30.1%.

Within Materials (+8.2%), with continued lithium price strength ahead of consensus forecasts the sector is moving towards the positive side led by Pilbara Minerals (PLS, +99.1%) and OZ Minerals (OZL, +45.6%).

Conversely, the worst performing sectors were Utilities (-16%) and Real Estate (-4.7%). Due to ongoing hikes in Interest rates and increasing Inflation both sectors experienced widespread decline. The largest fall came from AGL Energy (AGL, -16%), Centuria Capital Group (CNI, -15.2%) and Arena REIT (ARF, -21%).

Key Contributors

OZ Minerals (OZL, overweight) – the copper miner was a positive contributor to the portfolio during the month following BHP’s $25/share takeover offer for the company. The offer represented a 32% premium to prior close. With the OZL board rejecting the initial offer, we recognize the potential for BHP to return with a higher bid. The potential for a counterbidder to emerge is limited, in our view, given BHP’s significant regional synergies with Oz Minerals. We retain our fundamental positive view on OZL due to its two high quality, long life, 100% owned copper mines in South Australia - Prominent Hill and Carrapateena. We expect the company’s copper production to double to >200ktpa by 2030, as Carrapateena moves to a block caving operation, and the company develops the greenfield West Musgrave copper/nickel deposit in Western Australia.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Sept-2022.pdfAugust, 2022

Key Contributors

OZ Minerals (OZL, overweight) – the copper producer was a positive contributor to the portfolio during the period following BHP’s takeover offer for the company. The offer, priced at $25 per share, represented a 32% premium to the pre-bid price. With the OZL board rejecting the initial offer, we recognize the potential for BHP to return with a higher bid. The potential for a counterbidder to emerge is limited, in our view, given BHP’s significant available regional synergies. We retain our fundamental positive view on OZL due to its two high quality, long life, 100% owned copper mines in South Australia – Prominent Hill and Carrapateena. We expect the company’s copper production to double to >200ktpa by 2030, as Carrapateena moves to a block caving operation, and the company develops the greenfield West Musgrave copper/nickel deposit in Western Australia.

Pilbara Minerals (PLS, overweight) – the lithium producer was an outperformer during the period, with continued lithium price strength ahead of consensus forecasts. We believe PLS provides the most attractive exposure to lithium as a future facing commodity. The company’s flagship project, the Pilgangoora spodumene project, is well positioned to benefit from continued high lithium prices. The project is in the process of undertaking a 100ktpa capacity expansion to 680ktpa, with a clear path to 1,000ktpa through additional – and capital efficient – brownfield expansions. The company is progressing a downstream lithium hydroxide strategy with partner POSCO and assessing the potential to produce a value-added lithium/salts product.

Key Detractors

TPG Telecom (TPG, overweight) – the Australian telco underperformed during the period following a slightly disappointing (4% miss at the EBITDA level) result. We retain a positive view on the company given the mobile market is becoming more rational supporting repricing, as the value brand TPG can gain market share and technology shifts towards fixed wireless and fiber to the basement will favor TPG. We expect the momentum in the business to continue improving through F23 and the valuation remains attractive at 8 times EV/EBITDA.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Aug-2022.pdfJuly, 2022

Key Contributors

Megaport (MP1) – the company outperformed during the period after reporting a stronger than expected June quarter result across revenue growth (+10% quarter on quarter) and its first positive quarterly EBITDA result. We see strong growth from the core business connecting data centres to the cloud, with a strong global pipeline as businesses invest in IT projects. With its expansion into broader telecommunication services – which leverages the same infrastructure – the total addressable market more than doubles. While the company is currently at an inflection point for earnings and cashflow, we believe all metrics will turn positive in the next year offering significant long-term earnings and cashflow potential.

Nanosonics (NAN, overweight) – the disinfection medical device maker outperformed during the month as growth stocks found support following a period of underperformance. Our overweight position is premised on the company’s global market leadership in a large and growing addressable market. While growth rates had been interrupted by COVID and access to hospitals, access is now resuming and, following the transition of the GE distribution arrangement, we believe the company is well positioned to resume its long-term growth trajectory in the US and continue to develop new markets in the UK, Europe and Japan. Nanosonics has attractive economics with a high level of recurring revenue from consumables and upside from accelerating the upgrade cycle and new products.

Pinnacle Investment Management (PNI) – the investment manager outperformed during the period, supported by higher equity markets and the company reporting higher than expected performance fees. We remain positive on PNI going forward with continued inflows supported by strong products and international distribution, further margin expansion supported by the fixed cost nature of funds management businesses and new manager formation both organically and via acquisitions.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jul-2022.pdfJune, 2022

Key Contributors

Atlas Arteria (ALX, overweight) – the toll road operator outperformed due to its transparent inflation hedge and, moreover, as IFM’s global infrastructure fund took a 14.96% stake in the company, causing speculation of a possible takeover bid. We maintain an overweight position based on ALX’s strong liquidity and balance sheet position, discounted valuation and exposure to traffic recovery in Europe and the US. ALX trades on less than 11.0 times normalised EV/EBITDA, which sufficiently captures the disruption from COVID-19 as travel restrictions and lockdowns reduce traffic volumes in the short term. Beyond traffic normalisation, we see a path towards value creation for ALX through concession extensions at APRR achieved as a means of funding expansion projects and settling the Dulles Greenway tolling regime.

Key Detractors

Megaport (MP1, overweight) – the company underperformed following a weaker-than-expected 3Q22 update. Revenue grew 5% to $27.9mn for the quarter sequentially, slower than analyst forecasts, following its strategy to increase emphasis on indirect sales. We see the slower revenue growth as temporary based on the view the strategy shift is a short-term headwind but, in the long term, will likely create greater opportunities. We see strong growth from the core business connecting data centres to the cloud, with a strong pipeline in its key US geography as businesses invest in IT projects. With its expansion into telecommunication services – which leverages the same infrastructure – the total addressable market likely more than doubles. While the company is currently at an inflection point for earnings and cashflow we believe it will turn positive in the next year.

May, 2022

Key Contributors

Worley (WOR, overweight) – the engineering services firm outperformed due to expectations the global energy crisis will stimulate capex for both oil & gas and energy transition projects. We remain overweight the company. Following the Jacobs ECR acquisition, the business is diversified across different markets and, in our view, is well positioned to capture higher structural demand from energy transition work to low carbon solutions in addition to its traditional work for the oil & gas industry. We believe WOR’s valuation provides significant support at current levels, with the stock trading on 18.9 times forward earnings, a sharp discount to the Industrials ex-Financials at 25.5 times. Tabcorp (TAH, overweight) – the company contributed to excess returns as it demerged its lottery and wagering divisions during the month. The outcome supported our

Key Detractors

AUB Group (AUB, overweight) – the insurance broker underperformed after announcing the acquisition of London-based Tysers, a wholesale insurance broker, for up to $1,056mn. The deal is funded from a $350mn equity raising, a new $675mn debt facility and a $176mn placement to the vendor (with deferred consideration). We support the acquisition, which is highly EPS accretive (30% on a pro-forma basis for CY22) and offers new growth through global commercial insurance lines. More broadly we are overweight AUB on the grounds that its earnings are resilient in the current environment (mid-single digit premium rate rises) as the core business sees higher earnings growth via improved product and capacity offerings. As a result, we view the company’s valuation as attractive (18.4 times forward earnings), well below peer Steadfast (SDF) (22.5 times) but with stronger growth options.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-May-2022.pdfApril, 2022

Key Contributors

Flight Centre (FLT, overweight) – the travel services company outperformed as remaining international COVID restrictions were removed, allowing travel conditions to normalise. We remain overweight as we continue to see significant upside at current levels based our positive view of the Leisure division (38% of pre-COVID EBIT), which is set to benefit from pent-up travel demand in FY23 and FY24, with a skew towards bricks & mortar. In comparison, consensus is factoring Total Travel Value (TTV) remaining 30% below FY19 levels by FY24. And while Corporate (60% of pre-COVID EBIT) faces challenges from cost savings and a preference for Zoom meetings, FLT is taking market share in the segment. As a result, we see FLT as highly attractive at an EV/EBITDA of 12.3 times in FY23.

Key Purchases

Pilbara Minerals (PLS) – we established a position in the lithium producer during the period. We see PLS as the most attractive exposure to the future facing commodity. PLS’s flagship project, the Pilgangoora spodumene project, is well positioned to benefit from higher lithium prices as commercial production ramps up following the successful completion of Phase 1 construction. Further, PLS is assessing the potential to produce a value-added lithium/salts product, compared to spodumene concentrate currently, which we estimate could capture as much 70- 80% of the value in the supply chain. Flight Centre (FLT) – we increased our position in the travel services company during the period. We see significant upside at current levels based our positive view of the Leisure division (38% of pre-COVID EBIT), which is set to benefit from pent-up travel demand in FY23 and FY24, with a skew towards bricks & mortar. In comparison, consensus is factoring Total Travel Value (TTV) remaining 30% below FY19 levels by FY24. While Corporate (60% of pre-COVID EBIT) faces challenges from cost savings and a preference for Zoom meetings, FLT is taking market share in the segment. As a result, we see FLT as highly attractive at an EV/EBITDA of 12.3 times in FY23.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Apr-2022.pdfMarch, 2022

Key Contributors IGO Limited (IGO, overweight) – the EV commodities miner outperformed alongside the lithium price, with spodumene rising 10% to US$2,810/t. Its 1H22 result was mixed, with inaugural lithium guidance modestly below consensus on volumes but offset by higher pricing and a better-thanexpected performance from its Nova nickel asset. Our positive thesis remains premised on the miner’s recent US$1.4bn Greenbushes acquisition, its $A1.1bn takeover of nickel miner Western Areas (WSA) and its existing portfolio of high-quality assets. We support the Greenbushes acquisition for several reasons. Not only does it give IGO exposure to a high-quality, long-dated asset (>20 years mine life), but it also completes IGO’s suite of battery commodities with the company already producing nickel, copper and cobalt. We also think the purchase price was reasonable, with Greenbushes likely to be NPV and EPS accretive earlier than FY23. We support the WSA acquisition on the grounds it diversifies production (rebalancing

Key Detractors Nanosonics (NAN, overweight) – the disinfection medical device maker underperformed as the market focused on risks associated with its post-COVID recovery, specifically as the company shifts the sale of its consumables from its partner, GE, to its own direct channel. Our positive view towards the company remains premised on its leverage to the re-opening US economy and, moreover, the growing acceptance of its proprietary product, translating into higher earnings growth. NAN’s product, Trophon, is the global market leader with over 50% market share in North America. As regulatory change relating to disinfection protocols continues to drive adoption of NAN’s products, the sale of consumables for its devices generates a high-quality, annuity-style revenue stream. NAN also has a strong balance sheet – it is in a net cash position – to fund future growth and support ongoing product innovation.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Mar-2022.pdfFebruary, 2022

Key Contributors

Evolution Mining (EVN, overweight) – the gold miner outperformed alongside the commodity (+6% to $US1910/oz), which more than offset a softer 1H22 result and expectations for a heavy 2H22 skew (~53% of production) to meet full-year guidance. EVN is our preferred exposure within the S&P/ASX Midcap 50 Index, based on its diversified, high-quality assets and strong management team. While the growth outlook may not be as compelling as peer Northern Star (NST), we see upside based on the company’s production at Cowal and Red Lake assets and improving cost profile.

Key Detractors

Nanosonics (NAN, overweight) –the disinfection medical device maker underperformed as the market focused on risks associated with its post-COVID recovery, specifically as the company shifts the sale of its consumables from its partner, GE, to its own direct channel. Our positive view towards the company remains premised on its leverage to the re-opening US economy and, moreover, the growing acceptance of its proprietary product, translating into higher earnings growth. NAN’s product, Trophon, is the global market leader with over 50% market share in North America.

As regulatory change relating to disinfection protocols continues to drive the adoption of NAN’s products, the sale of consumables for its devices generates a high-quality, annuity-style revenue stream. NAN also has a strong balance sheet – it is in a net cash position – to fund future growth and support ongoing product innovation.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Feb-2022.pdfJanuary, 2022

The Emerging Leaders Benchmark declined 8.8% during the month, underperforming the broader ASX300’s -6.5% return and taking its 12-month return to +9.4%. Globally, the S&P500 and MSCI World Index returned -5.2% and -4.9% respectively as US real yields rose, with the US 10-year Treasury Inflation-Protected Securities (TIPS) climbing 38 bps to -0.69% as the US Fed said it would likely start to increase interest rates in March. At a sector level, high-PE cohorts within Health Care (- 16.7%) and Information Technology (-14.9%) recorded the most significant declines, led by companies with long-dated cash flows like Wisetech Global (WTC, -22.7%), Altium (- 21.0%) and Pro Medicus (PME, -27.8%). Gold (-13.7%) also declined significantly given its negative correlation with real interest rates. Conversely, Energy (-0.7%) was the strongest performer as Brent Crude lifted by 18% to US$92/bbl. Oil & Gas producer Beach Energy (BPT, +17.5%) and engineering services company Worley (WOR, +8.7%) were among the top performers. Utilities (+7.7%) also outperformed during the period amid the outlook for higher electricity prices, supported by AGL Energy (AGL, +15.6%).

Key Contributors:

IGO Limited (IGO, overweight) – the EV commodities miner outperformed alongside the lithium price, with spodumene rising 6% to US$2,710/t. Our positive thesis remains premised on the miner’s recent US$1.4bn Greenbushes acquisition, its A$1.1bn takeover of nickel miner Western Areas (WSA) and its existing portfolio of high-quality assets. We support the Greenbushes acquisition for several reasons. Not only does it give IGO exposure to a highquality, long-dated asset (>20 years mine life), but it also completes IGO’s suite of battery commodities with the company already producing nickel, copper and cobalt. We also think the purchase price was reasonable, with Greenbushes likely to be NPV and EPS accretive earlier than FY23. We support the WSA acquisition on the grounds it diversifies production (rebalancing commodity exposure to 70% Li, 30% Ni) and extends the mine life for nickel production (which is currently through its world-class Nova asset).

Key Detractors:

Megaport (MP1, overweight) – the company underperformed after giving a 2Q22 update which revealed higher costs as the business adjusts its operating model to focus on its indirect sales channel. We view the pick-up in costs as supporting an acceleration in executing on the growth opportunity and remain overweight the stock, premised on strong growth from the core business connecting data centres to the cloud, with a strong pipeline in its key US geography as businesses invest in IT projects. With its expansion into telecommunication services – which leverages the same infrastructure – the total addressable market more than doubles. While the company is currently at an inflection point for earnings and cashflow we believe it will turn positive in the next year. We do not believe MP1’s strong and sustainable revenue growth outlook is reflected in its share price.

December, 2021

Key Contributors

IGO Limited (IGO, overweight) – the battery materials producer outperformed alongside the lithium price. We remain overweight the company. Our positive thesis is premised on its US$1.4bn Greenbushes acquisition and its existing portfolio of high-quality assets. We support the acquisition for several reasons. Not only does it give IGO exposure to a high-quality, long-dated asset (>20 years mine life), but it also completes IGO’s suite of battery commodities with the company already producing nickel, copper and cobalt. We also think the purchase price was reasonable, with Greenbushes likely to be NPV and EPS accretive earlier than FY23. We also hold a positive view of IGO’s Nova asset – a world-class reserve which supports an increasing production profile.

Key Detractors

Select Harvests (SHV, overweight) – the almond producer retraced strong outperformance as stubbornly low almond prices (to below mid-cycle levels) overshadowed a strongerthan-expected FY21 result. We remain overweight SHV, with our positive view based on several factors. Firstly, we see considerable upside to sales from both pricing (pre-COVID19 was at A$8.50/kg) and volume (which should grow by +5% per annum over the next two years as orchards mature). Secondly, we expect costs to decline from abnormally high levels, with water prices likely to fall as drought conditions recede. Thirdly, limited value is currently implied in SHV’s food processing business, which it is realising value through capital releases. Lastly, SHV has a solid balance sheet and supportive valuation, with hard assets comprising more than 70% of the company’s enterprise value.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Dec-2021.pdfNovember, 2021

The Emerging Leaders Benchmark rose 0.5% during the month, outperforming the broader ASX300’s -0.5% return and taking its 12-month return to 19.4%. Globally, equities declined late in the period (MSCI World Index -1.4% for November) as the COVID variant, labelled Omicron, drove uncertainty around the growth outlook. Further, persistent inflation in the US continued to stoke concerns about faster tapering and US interest rate rises

Key Contributors Link Administration (LNK, overweight) – the share registry company outperformed after receiving several takeover offers during the period and giving a positive trading update. US-based Carlyle group returned with a $5.38 per share offer, which included a cash component for the base business and a pro-rata distribution of LNK’s PEXA stake. Meanwhile, LNK received two bids for its Banking and Credit Management (BCM) business. The second offer – at €65m – came from Ireland-based LC Financial Holdings. LNK also gave a trading update during the period, reaffirming full-year guidance and commenting that year-to-date trading has been ahead of expectations. We remain overweight as the corporate activity supported our view of the latent value in the business. We hold a positive view of PEXA premised on the infrastructure-like characteristics of the property settlement exchange upon maturity, supplemented by numerous growth opportunities in immediate adjacencies. Further, LNK is positively leveraged to higher US interest

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Nov-2021.pdfOctober, 2021

The Emerging Leaders Benchmark rose 0.6% during the month, taking its 12-month return to 28.9%. The local index underperformed global indices – with the MSCI World Index returning 5.5% – as Australian 10-year bond yields lifted 59 bps to 2.08% during the period on expectations the RBA would hike rates earlier amid inflation pressure. Gold (+10.2%) was the top performer during the period, with the sector seen as a beneficiary of stronger inflation. Within the sector, Silver Lake Resources (SLR, +26.5%) and West African Resources (WAF, +34.0%) were the strongest contributors to the benchmark’s return

Key Contributors

IGO Limited (IGO, overweight) – the battery mineral producer outperformed as lithium prices continued to strengthen, with spodumene rising 2% to $US2,300/t, on top of the 92% rise in the prior month. Our positive view is premised on the recent Greenbushes acquisition, which gives IGO exposure to a high-quality, long-dated asset (>20 years mine life) and completes its suite of battery commodities with the company already producing nickel, copper and cobalt. We also think the purchase price was reasonable, with Greenbushes likely to be NPV and EPS accretive by FY23. We also hold a positive view of IGO’s Nova asset – a world-class reserve which supports an increasing production profile

Key Detractors

Star Entertainment (SGR, overweight) – the casino operator underperformed in response to media allegations that it had enabled suspected money laundering, fraud and foreign interference. Following the allegations, the company announced that the Liquor and Gaming Authority’s regular review of The Star Sydney would now also incorporate public hearings. We reduced our position in the company following the media allegations. We had taken some comfort from SGR having undergone several recent reviews without any major issues identified, in stark contrast to Crown Resorts (CWN). However, the allegations raise the risk profile of the stock, introduces the possibility there may be sanctions against the company, and may remove potential upside opportunities (extra gaming licences, concessions). We are engaging extensively with management and are undertaking further independent validation in relation to the allegations, which the company has labelled as misleading

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Oct-2021.pdfSeptember, 2021

The S&P/ASX Emerging Leaders Benchmark lifted by 3.7% in the quarter, taking its 12-month return to +32.3%. In comparison, the broader ASX 300 returned 1.8% and the MSCI Global Index returned 0.7% in local currency terms. However, FY21 reporting season saw more misses than beats despite recording +28% growth y/y, and FY22 forecasts were revised down at -1.2% for the ASX200 and - 1.5% for the Small Ords

Key Contributors

Carsales.com (CAR, overweight) – the online automotive company outperformed as its FY21 result came in at the top end of guidance issued in May, with revenue and NPAT growing 4% and 11% respectively y/y. While prolonged lockdowns in NSW and VIC clouds the outlook for FY22, CAR still expects ‘solid growth’ in underlying NAPT. A new product launch called “carsales SELECT” – a digital offering times in FY23), with hard assets comprising more than 70% of the company’s enterprise value

Key Detractors

Wisetech Global (WTC, underweight) – the logistics software company outperformed after delivering a strongerthan-expected FY21 result. EBITDA grew 63% to $207mn, 13% ahead of consensus expectations, as demand accelerated for WTC’s software platform and margins expanded on cost initiatives. We remain underweight WTC based on the company’s unappealing valuation and high risk profile following a string of acquisitions. WTC now trades at a forecast EV/Sales of 24.2 times, which we believe continues to capitalise unrealistic growth expectations and ignores downside risks.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Sept-2021.pdfAugust, 2021

The S&P/ASX Emerging Leaders Benchmark lifted by 4.4% in August, taking its 12-month return to +30.2%. In comparison, the broader ASX300 Index returned 2.6% and the MSCI Global Index returned 2.7%. However, FY21 reporting season saw more misses than beats despite recording +28% growth y/y, and FY22 forecasts were revised down at -1.2% for the ASX200 and -1.5% for the Small Ords1 . Nevertheless, equity valuations rose globally amid lower bond yields, with the US 10-year bond yield declining 21 bps to 1.23% in response to dovish commentary from the US Fed and the Australian 10-year bond yield flat at 1.16%.

Key Detractors Wisetech Global (WTC, underweight) – the logistics software company outperformed after delivering a strongerthan-expected FY21 result. EBITDA grew 63% to $207mn, 13% ahead of consensus expectations, as demand accelerated for WTC’s software platform and margins expanded on cost initiatives. We remain underweight WTC

Key Contributors Nanosonics (NAN, overweight) – the disinfection medical device maker outperformed after beating expectations with its FY21 result. A strong recovery in 2H21 saw revenue up

based on the company’s unappealing valuation and high risk profile following a string of acquisitions. WTC now trades at a forecast EV/Sales of 23.7 times, which we believe continues to capitalise unrealistic growth expectations and ignores downside risks.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Aug-2021-1.pdfJuly, 2021

Australian shares rose modestly in July despite ongoing lockdowns across the east coast of the country.

The Emerging Leaders Benchmark returned 0.7% for the month, taking its 12-month return to 33.1%. However, the market lagged overseas indices, with the S&P500 returning 2.4% during the month amid an upbeat US corporate earnings season.

Metals & Mining ex-Gold (+12.1%) was the top contributor to the index, supported in most part by miners leveraged to the electric vehicle theme, including IGO Limited (IGO, +22.0%), Lynas Corporation (LYC, +28.6%), Pilbara Minerals (PLS, +22.1%), Orocobre (ORE, +27.5%) and Galaxy Resources (GXY, +27.0%).

Corporate activity increased across the broader market during the period. Australian Pharmaceutical Industries (API, +26.5%) received a takeover bid from Wesfarmers (WES) at $1.38 per share (all-cash), a 21% premium to its last-traded share price prior to the announcement. Elsewhere, Tabcorp (TAH, -4.4%) rejected a third takeover bid for its wagering & media business, instead choosing to spin off its lotteries division.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jul-2021.pdfJune, 2021

Australian small caps shrugged off new COVID-19 outbreaks across the country to deliver strong returns in the June quarter.

The Emerging Leaders Benchmark increased by 9.3% in the three months to 30 June 2021, taking its 12-month return to 34.5%. The benchmark was in line with the broader ASX300 for the period and outperformed global indices, with the MSCI World Index returning 7.7%, despite all major cities going into lockdown at one point during the quarter in response to COVID-19 cases.

Health Care (+12.7%) was the top performing sector, supported by ResMed (RMD, +30.0%) given its leverage to the re-opening US economy, as well as companies including Pro Medicus (PME, +42.1%), Ansell (ANN, +10.9%) and Healius (HLS, +13.5%). Elsewhere, Industrials (+12.4%) was supported by a disparate group of companies including Reece (REH, +37.7%), ALS (ALQ, +36.3%) and Cleanaway Waste Management (CWY, +20.0%).

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jun-2021.pdfMay, 2021

Gold (+13.1%) outperformed alongside the commodity, up 7.5% during the period to $US1,900/oz. At a stock level the largest benchmark contributors included Northern Star (NST, +11.3%), Evolution Mining (EVN, +16.9%) and Perseus Mining (PRU, +18.4%).

Elsewhere, REITs (+2.0%) were supported by UnibailRodamco-Westfield (URW, +7.2%), Ingenia Communities Group (INA, +5.7%) and Waypoint REIT (WPR, +4.0%). Within Consumer Discretionary (+1.4%) Corporate Travel Management (CTD, +12.7%) was seen as a beneficiary of the US re-opening, more than offsetting Flight Centre (FLT, - 9.1%) which declined amid new border closures in Australia. Conversely, within Information Technology (-6.0%) EML Payments (EML, -41.9%) faced pressure after an Irish regulatory body raised concerns about its PFS Card Services business, while Nuix (NXL, -33.1%) announced its 2nd downgrade in two months following its IPO in December 2020.

Consumer Staples (-4.3%) was weighed down largely by Costa Group (CGC, -27.0%). The horticultural company announced 1H21 earnings would only be marginally above the previous year, despite cycling a weak 1H20 and reporting significant growth in 2H20

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-May-2021.pdfApril, 2021

Australian small and midcaps outperformed large cap peers in April as Tech, Industrials and miners supported returns. The Emerging Leaders Benchmark returned +5.1% for the month, taking its 12-month return to +42.7%. The index outperformed the broader ASX300, which returned +3.7% during the period.

Gold (+13.3%) and Information Technology (+8.6%) were the top performing sectors as the ‘reflation trade’ partially reversed, with the Australian 10-year bond yield falling 10 bps to 1.69%. Within the former, De Grey Mining (DEG, +48.2%) and Chalice Mining (CHN, +32.9%) released promising drilling results. Within tech, top performers included NEXTDC (NXT, +11.2%), Altium (ALU, +12%), Megaport (MP1, +29.7%) and EML Payments (EML, +16.5%). Elsewhere, lithium miners rallied heavily, led by Galaxy Resources (GXY, +55.3%) and Orocobre (ORE, +41.8%) as the two companies announced a $4bn merger during the period. Within Industrials, waste management company Cleanaway Waste Management (CWY, +29.5%)

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Apr-2021.pdfMarch, 2021

Australian equities rose modestly in the March quarter as a stronger-than-expected reporting season more than offset rising bond yields globally. The Emerging Leaders benchmark increased 1.1% for the quarter, taking its 12-month return to +56.4%. In comparison, the broader ASX 300 returned 4.2% for the quarter and 38.3% for the year. Returns had been stronger as companies delivered one of the best reporting seasons on record, with 3.2 times more beats than misses1 . However, equities de-rated in the second half of the period as the Australian 10-year bond yield rose 82 bps to 1.79%.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Mar-2021.pdfFebruary, 2021

Australian equities were flat in February as rising bond yields globally offset a stronger-than-expected reporting season.

The Emerging Leaders benchmark increased 0.08% for the month, taking its 12-month return to 19.1%. In comparison, the broader ASX 300 returned 1.5% for the month and 7.1% for the year. Returns had been stronger as companies delivered one of the best reporting seasons on record, with 3.2 times more beats than misses1 . However, equities derated in the second half of the month as the Australian 10- year bond yield rose 73 bps to 1.88%.

As beneficiaries of the higher bond yield environment, regional banks (+15.6%) were among the strongest performers in the benchmark. Further, Bank of Queensland (BOQ, +13.6%) announced the acquisition of ME Bank – increasing its loan book by 57% – while Bendigo and Adelaide Bank (BEN, +9.1%) delivered a strong 1H21 result, supported by very low impairment charges and strong lending growth

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Feb-2021.pdfJanuary, 2021

Key Contributors

Bingo Industries (BIN, overweight) – the waste management company outperformed after receiving a nonbinding indicative takeover offer from a consortium comprising CPE Capital and Macquarie Infrastructure and Real Assets (MIRA). The proposal came in two forms: a cash offer at $3.50 per share, representing a 28% premium to last close, or a mix of cash and unlisted scrip at a lower upfront cash price. We remain overweight based on our positive long-term view of the company, which we see as attractive at current levels regardless of the outcome of the takeover bid. As the waste management environment normalises, BIN is well positioned to take market share given its vertically integrated business model, attractive growth projects (particularly within Infrastructure) and interstate expansion opportunities.

prioritise the trade sale process of PEXA, which in our view will unlock material value.

Beach Energy (BPT, overweight) – the oil & gas producer underperformed during the period after announcing a slightly weaker-than-expected 1Q21 result. Production came in 4-6% below analyst forecasts at 6.2MMboe, with the miss due to a number of factors including scheduled maintenance, unscheduled downtime and natural field declines. Nevertheless, FY21 guidance was unchanged at 26-28.5MMboe. We established a position in the company earlier in the period based on several factors. We see its valuation as appealing at an FY22 P/E of 10 times and 3.5 times EV/EBITDA, underpinned by low-risk gas contracts (which are likely to re-price higher) and its tangible organic growth platform (funded by a robust balance sheet). While FY21 and FY22 remain investment years for BPT to shore up future production volumes (Otway, Cooper, Western Flank), we see the medium-term investment proposition as attractive. We also support BPT’s mandate to grow through further accretive M&A, the execution of which will likely require further equity.

Key Purchases Beach Energy (BPT) – we established a position in the oil & gas producer during the period. We see BPT’s valuation as appealing at an FY22 P/E of 10 times and 3.5 times EV/EBITDA, underpinned by low-risk gas contracts (which are likely to re-price higher) and its tangible organic growth platform (funded by a robust balance sheet). While FY21 and FY22 remain investment years for BPT to shore up future production volumes (Otway, Cooper, Western Flank), we see the medium-term investment proposition as attractive. We also support BPT’s mandate to grow through further accretive M&A, the execution of which will likely require further equity.

Carsales.com (CAR) – we increased our position size in the automotive online classifieds company during the period. In the short term we expect demand for second-hard cars to remain elevated in both Australia and South Korea, driving upside to earnings versus consensus forecasts. In the long term our positive view is premised on the belief CAR should benefit from attractive earnings growth, conservative accounting (with low capitalisation of research and development investment) and undervalued international businesses

Key Sales Incitec Pivot (IPL) – we reduced our position in the explosives and fertiliser maker following recent outperformance, but remain overweight. Our positive view remains premised on key commodities (urea and DAP) reverting to mid-cycle levels. Furthermore, other factors which had weighed on performance throughout FY19 and FY20 – weather-related issues, plant outages and COVIDrelated disruption – are now largely behind the company. Lead indicators suggest higher demand for the commodities and the explosives business is experiencing

Nanosonics (NAN) – our positive view towards the medical disinfection device company is premised on the growing acceptance of its proprietary product translating into higher earnings growth. NAN’s product, Trophon, is the global market leader with over 50% market share in North America. As regulatory change relating to disinfection protocols continues to drive adoption of NAN’s products, the sale of consumables for its devices generates a high-quality, annuity-style revenue stream. NAN also has a strong balance sheet – it is in a net cash position – to fund future growth and support ongoing product innovation

Key Active Underweights

Northern Star (NST) – we were underweight NST based on its stretched valuation metrics, at 6.7 times forward EV/EBITDA, and negative long-term view of the gold price. While we are positive towards the company’s operations and its proposed merger with Saracen Minerals (SAR), we see significant downside risk to the commodity – at elevated levels of $US1,800oz – amid an outlook for higher real interest rates (which are generally a headwind to the gold price). We maintain a small exposure to gold through diversified miner IGO Limited (IGO).

Tabcorp (TAH) – we are underweight the gambling services provider because we believe earnings expectations are too optimistic and regard the market’s valuation, at 24.3 times 12-month forward P/E, as stretched. Our key concern is the outlook for the conventional wagering business, which operates in a low growth industry and with high levels of competition, placing intense pressure on its traditional retail distribution strategy.

Evolution Mining (EVN) – we are underweight EVN based on its stretched valuation metrics, at 7.4 times forward EV/EBITDA, and negative long-term view of the gold price. While we are positive towards the company’s operations, we see significant downside risk to the commodity – at elevated levels of $US1,800oz – amid an outlook for higher real interest rates (which are generally a headwind to the gold price). We maintain a small exposure to gold through diversified miner IGO Limited (IGO).

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Jan-2021.pdfDecember, 2020

Australian equities rose alongside global markets in the December 2020 quarter, driven by positive vaccine news, higher commodity prices and a decisive US election outcome.

The Emerging Leaders Benchmark returned 15.4% for the quarter, taking its 2020 return to +13.1%. In comparison, the broader ASX 300 returned 13.8% for the quarter and +1.7% for the year. Markets surged globally after three major COVID-19 vaccine candidates were announced as highly effective in extensive trials, and after Joe Biden was declared the winner of the US Presidential Election.

Sectors which were hit hardest by COVID-19 rallied sharply. Energy (+24.8%) was the strongest performer as Brent Crude lifted 29% to US$52 per barrel, led by Worley (WOR, +20.3%) and Beach Energy (BPT, +36.7%).

Other strong performers included the Regional Banks (+46.9%), Retail REITs (+23.8%) and Media & Entertainment (+24.6%). Consumer Discretionary (+11.4%) also rallied, though it faded late in the quarter as border restrictions were reimposed across Australia in response to new COVID clusters. Conversely, sectors which had proved resilient during the downturn – Gold (-11.4%), Utilities (+1.0%) and Health Care (+4.6%) – underperformed. At a stock level, the worst performers included Regis Resources (RRL, -25.3%) and Mesoblast (MSB, -55.7%). Information Technology (+19.4%) was the exception, driven by Afterpay (APT, +47.5%) as the Buy-Now, Pay-Later market leader entered the S&P/ASX 20 Index.

File: https://commentary.quantreports.net/wp-content/uploads/2020/12/Yarra-Emerging-Leaders-Fund-Dec-2020.pdfNovember, 2020

Key Contributors

Worley (WOR, overweight) – the engineering services company outperformed after Brent Crude increased by 27% during the period. We continue to believe WOR is in a strong position to withstand an economic slowdown and lower oil prices, with significant refinancing headroom and business diversification across different markets. We believe WOR’s valuation provides significant support at current levels, with the stock trading on 15.4 times two-year forward earnings – a cyclical low multiple despite its more resilient earnings base.

Nanosonics (NAN, overweight) – the disinfection medical device maker outperformed during the period after issuing a well-received trading update. Both its consumables and hardware business lines have rebounded FY21 to date from the COVID-impacted months of FY20, with sales up +25% and +16% respectively. Despite US hospitals handling record COVID cases, second-wave impacts have been less severe due to better equipment and preparation. We remain overweight the company, premised on the growing acceptance of its proprietary product translating into higher earnings growth. NAN’s product, Trophon, is the global market leader with over a 50% market share in North America. As regulatory change relating to disinfection protocols continues to drive adoption of NAN’s products, the sale of consumables for its devices generates a high-quality, annuity-style revenue stream. NAN also has a strong balance sheet – it is in a net cash position – to fund future growth and support ongoing product innovation

Northern Star Resources (NST, overweight) – the gold miner underperformed as the commodity declined 6% to

$US1,763 per ounce during the period. We were underweight NST based on its stretched valuation metrics (6.3 times forward EV/EBITDA), with our preferred exposures Regis Resources (RRL), Saracen Minerals (SAR) and diversified miner Independence Group (IGO). However, NST has announced a merger with SAR, with SAR shareholders receiving 0.3763 NST shares for every SAR share. We see the business combination as logical, with highly complementary operations (the Superpit joint venture) and organisational cultures, and the synergy metrics as attractive (A$1.5-2.0bn pre-tax NPV). On valuation, we see the potential for the combined group to re-rate to peer Newcrest Mining (NCM, 6.6 times forward EV/EBITDA) given its comparable size and growing production profile in Western Australia and Alaska.

Key Detractors

Saracen Minerals (SAR, overweight) – the gold miner underperformed as the gold price declined 6% to $US1,763 per ounce during the period. We remain overweight following the company’s announced merger with Northern Star Resources (NST). We see the business combination as logical, with highly complementary operations (the Superpit joint venture) and organisational cultures, and the synergy metrics as attractive (A$1.5-2.0bn pre-tax NPV). On valuation, we see the potential for SAR/NST to re-rate to peer Newcrest Mining (NCM, 6.6 times forward EV/EBITDA) given its comparable size and growing production profile in Western Australia and Alaska.

NEXTDC (NXT, overweight) – the data centre operator partially retraced prior outperformance despite reaffirming its FY21 guidance during the period. Management expects underlying EBITDA in the range of $125-130mn next financial year, up 20-24% y/y. We continue to believe NXT is structurally set to benefit from increasing adoption of cloud technology, and is accelerating its expansion to meet client demands by building new data centres which will support significant medium to longer term earnings growth.

Elders (ELD, overweight) – the agribusiness company partially retraced strong outperformance from prior periods despite delivering a better-than-expected FY20 result. EBIT came in at $119.4mn – 8% ahead of forecasts – largely due to market share gains in livestock and a higher real estate contribution. While the company didn’t provide earnings guidance, it reiterated its target for 5-10% EBIT and EPS growth through the cycle and a ROIC of 15%. We remain overweight the company. We are supportive of its recent acquisition of Australian Independent Rural Retailers (AIRR), which expands ELD into the rural merchandise market and is expected to be earnings accretive in FY21. More broadly, we continue to see cyclical upside, the potential for further accretive acquisitions, a simplified capital structure relative to prior years and modest valuation. The company has strong corporate appeal given its attractive business segments, and we see its 12-month forward P/E multiple of 13.3 times as supportive.

October, 2020

Australian shares rose sharply in October as euphoria around global economic growth and political initiatives drove the asset class higher, with small and mid-caps outperforming large caps. The Emerging Leaders Benchmark lifted 5.9% – its best monthly return since July 2016 – with all sectors making a positive return in the period. The performance was well above the 4.0% return the S&P/ASX 200 delivered and the 2.6% rise from the MSCI World Index. However, much of the excitement was overseas. Economic conditions continued to improve in Europe despite political tension in Spain, the US quarterly reporting season was better than expected and confidence grew that President Trump would be able to enact his tax cut initiatives. Domestically the environment was mixed: labour force data was strong with total employment rising by 3.1% year-on-year for September (its strongest rate since 2008) but retail sales were weaker than anticipated for August, up 2.1% year-on-year. At a sector level, Materials (+6.8%) was the top contributor to return as Metals & Mining rose 7.4% in the period. While most stocks made positive returns, lithium producers Galaxy Resources (GXY, +32.7%) and Pilbara Minerals (PLY, +27.6%) were the top performers. The highest contributor to return was Bluescope Steel (BSL, +17.0%) amid the outlook for wider steel spreads. Consumer Staples (+14.5%), however, was the top performing sector. The sharp rise was entirely due to stocks exposed to the Chinese demand theme, namely A2 Milk (A2M, +30.0%), Bellamy’s Australia (BLY, +59.9%), Blackmores (BKL, +35.4%) and BWX (+26.2%). In contrast, the worst performers were Utilities (+1.7%) and Financials (+2.4%). In the latter Bendigo and Adelaide Bank (BEN, -2.0%) weighed on performance after disappointing the market with its 1H18 guidance for net interest margins (NIM).

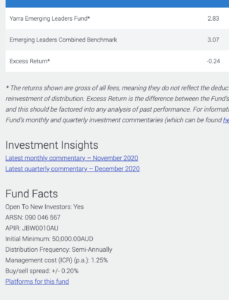

File:ticker: JBW0010AU

commentary_block: Array

factsheet_url:

https://www.yarracm.com/australian-equities/yarra-emerging-leaders-fund/

release_schedule: Monthly

fund_features:

Yarra Emerging Leaders Fund aims to achieve medium-to-long term capital growth by investing in small and medium sized Australian companies that are considered to possess strong capital-growth potential. In doing so, the Funds aim to outperform the benchmark over rolling three-year periods.

- The fund, substantially through its investment in the Emerging Leaders Pooled Fund, invests in securities which are listed on the ASE, but are not included in the S&P/ASX 50 Leaders Index.

- Fund benchmark: Emerging Leaders Combined Benchmark, comprising S&P/ASX Midcap 50 Accumulation Index and S&P/ASX Small Ordinaries Accumulation Index.

manager_contact_details: Array

asset_class: Domestic Equity

asset_category: Australian Multi-Manager

peer_benchmark: Domestic Equity - Multi-Manager Index

broad_market_index: ASX Index 200 Index

structure: Managed Fund